Programmable Money

Four Scenarios

June 30, 2026

No posts

“Central banks will have absolute control on the rules and regulations that will determine the use of that expression of central bank liability [currency] and also we will have the technology to enforce that.”

~ Agustín Carstens, “Cross-Border Payments—A Vision for the Future” (October 2020)

By Catherine Austin Fitts

A major, multipronged push is underway by both public and private players to move currency, bank deposits, and stocks and bonds onto distributed ledgers (digital transaction databases “stored and synchronized across multiple sites, institutions, or geographies”). There, the potential exists to make the transactions programmable—that is, able to use smart contracts and vulnerable to third-party rules and control. Central bank digital currencies (CBDCs) are programmable, but so are stablecoins and digital tokens being used to add these features to currencies and financial assets.

What are the goals of the fast-moving push for programmability? To answer that question, a useful tool is scenario planning—a strategic planning method that makes it possible to envision and prepare for multiple plausible futures.

Before we present our scenarios, however, we need to define a handful of key terms.

Two-lock transactions: In a basic two-lock transaction (for example, a cash transaction), the buyer and seller each have a “lock”—that is, each has the power to agree to or veto the transaction. If both buyer and seller agree, the two locks “click,” and the transaction proceeds. No third parties are involved.

Three-lock transactions: In the U.S., “know your customer” (KYC) regulations and the anti-money laundering (AML) provisions of the Bank Secrecy Act impose reporting and other requirements on financial institutions. These and other regulations have introduced a third “lock” into the banking system. The stated aim of these requirements is to keep banks from allowing transactions by “bad actors,” but the third lock has also metastasized to the retail level. In recent years, we have seen the rise of phenomena such as “debanking” (the “sudden and often unexplained closure of individuals’ or organizations’ financial accounts”) as well as other mechanisms and pretexts for denying transactions. Debanking’s “cascading effects,” says Thomson Reuters, “demonstrate the profound power that financial institutions hold in determining who can fully participate in the modern economy.”

Automated third lock: Until recently, third-lock intercession has been “manual” in the sense of requiring compliance by human beings, one by one, at thousands of financial institutions. However, the advent of technologies that permit granular “one person at a time” surveillance, as well as AI and the hyperscale data centers that support it, now make an automated third lock possible. Complex algorithms can be built into currency (or even into digital wallets) so that code, rather than human beings, becomes the gatekeeper of all financial transactions.

Technocracy: Technocracy is a system to implement central resource management and control through micromanagement by rules and algorithms. Although technocracy’s progenitors first envisioned their technocratic system of global control over a century ago, it is the digital systems and AI introduced in the 21st century that are making technocratic control mechanisms like programmability and an automated third lock possible.

The “whipping machine”: In his 2014 book, The Half Has Never Been Told: Slavery and the Making of American Capitalism, author Edward E. Baptist describes how slavery’s “entrepreneurs” perfected the application of whipping and other systematized forms of physical torture to increase slaves’ profitability and productivity, making torture a “factor of production.” In Baptist’s telling, the “whipping machine” has become a broader metaphor for the use of technology “to force people to focus their minds on inventing new ways to perform repetitive and mind-numbing labor at nearly impossible speed.” In our fourth scenario below, central bankers replace slavers, using the automated third lock to enforce central control over labor, travel, capital, and resources in a manner that can shift ownership and control of time and assets and extract labor and value.

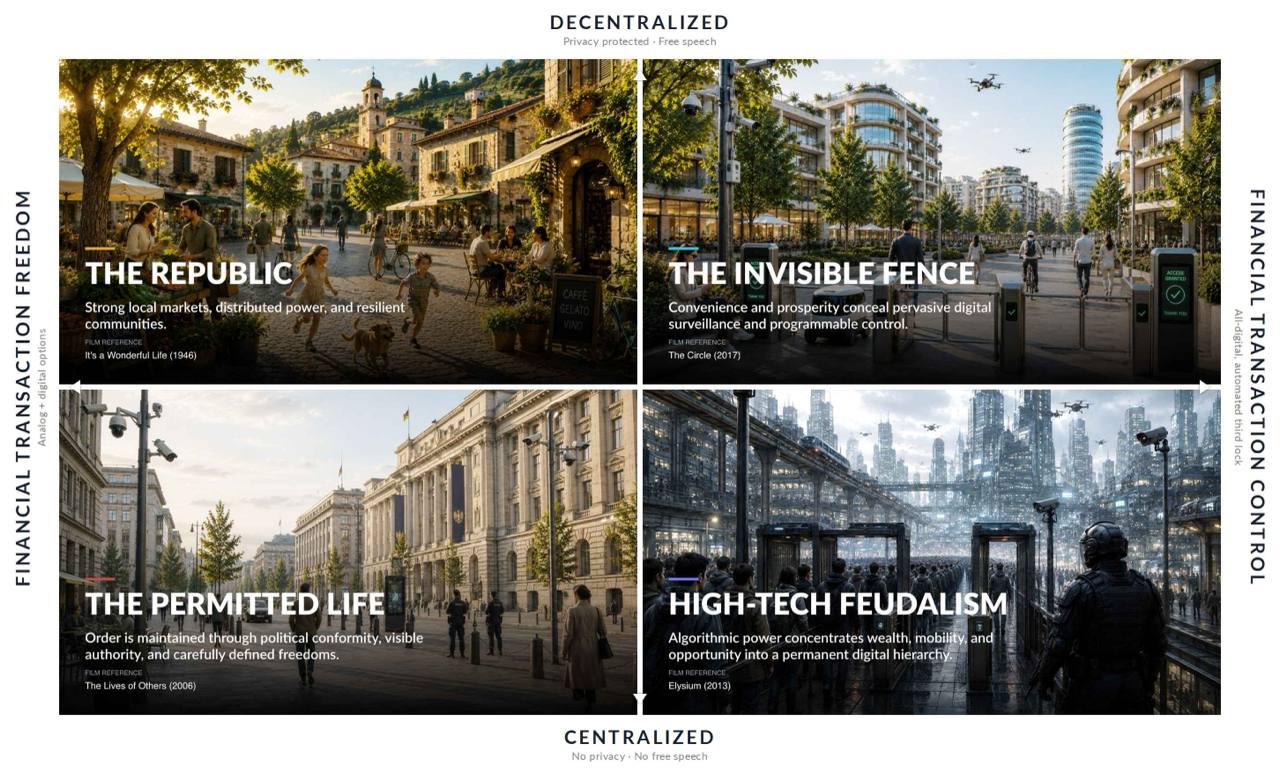

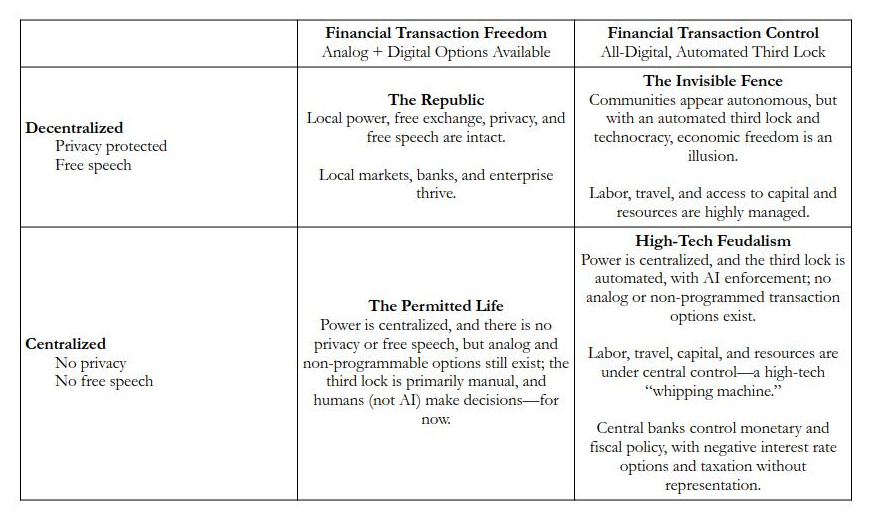

Four possible programmable money scenarios (see Table 1) that attempt to frame the intent of the people and institutions implementing these systems result from the intersection of two expressions of two variables:

Table 1. Four Programmable Money Scenarios

The Republic (Decentralized – Financial Transaction Freedom) represents the founding vision of distributed power combined with genuine economic freedom. Politics and economics are local—communities govern themselves, accountability flows through constitutional structures, and human beings make the decisions that affect other human beings. Privacy is protected, free speech is robust, and local markets and enterprise thrive. Individuals have real choices among analog and digital options for financial transactions. No automated third lock constrains what people can buy, sell, or save. This is the scenario to defend or restore—the baseline against which all others are measured. This is a high-trust society.

See it in film: It’s a Wonderful Life (1946)

The Invisible Fence (Decentralized – Financial Transaction Control) is a dangerous scenario precisely because it is the most likely to be marketed as “freedom.” Communities appear autonomous. Free speech and privacy nominally survive. Decentralization looks intact. But the financial transaction layer has been captured—an all-digital technocracy with an automated third lock means that economic freedom is an illusion. You can speak freely; you cannot act or transact freely. Labor, travel, and access to capital and resources are highly managed. Your ability to transact, accumulate, or exit is governed by terms and conditions rather than constitutional rights. The cage is invisible because it is built into the infrastructure, not announced as policy. Private payment stablecoins and programmable money systems that appear pro-freedom may in practice deliver this scenario. This is a low-trust society.

See it in film: The Circle (2017)

The Permitted Life (Centralized – Financial Transaction Freedom) combines centralized political and economic power with the absence of privacy and free speech, but preserves—for now—some degree of financial transaction freedom. Analog and non-programmable options still exist. People can still transact outside the fully digital system. However, this residual freedom functions as a managed release valve, not a right: it is tolerated by the central authority because removing it entirely would cause disruption, not because the authority lacks the will or capability to close it. The window can be closed at any time. This scenario has historical precedents in certain predigital authoritarian economies, which permitted cash and informal markets within limits. The critical question is always: what will trigger the closing of the window? This is a low-trust society.

See it in film: The Lives of Others (2006)

High-Tech Feudalism (Centralized – Financial Transaction Control) represents full-spectrum convergence: centralized political and economic power, no privacy, no free speech, no analog exits, and automated third-lock AI enforcement of every financial transaction. No analog or non-programmed transaction options exist. The Constitution is effectively subordinated to code and terms of service. Labor, travel, and access to capital and resources are under central control and are used to extract value in a high-tech “whipping machine.” AI and software algorithms make material decisions about who can transact, on what terms, and for what purposes—without human accountability and without legal recourse. Nothing inside the system is voluntary; nothing outside the system is possible. The feudal analogy is precise: serfs were not always legally prohibited from owning property, but their practical ability to accumulate, transfer, or exit was controlled by the lord. The technology changes the mechanism; the power relationship is ancient. Central banks control monetary and fiscal policy, with negative interest rate options and taxation without representation. This is a no-trust society.

See it in film: Elysium (2013)

Watch Agustín Carstens—General Manager of the Bank for International Settlements (BIS) from December 2017 to June 2025—describe the central bankers’ perspective on programmable money:

Already a subscriber?

Our mission is to help you live a free and inspired life. This includes building wealth in ways that build real wealth in the wider economy. We believe that personal and family wealth is a critical ingredient of both individual freedom and community, health and well-being.

Nothing on The Solari Report should be taken as individual investment, legal, or medical advice. Anyone seeking investment, legal, medical, or other professional advice for his or her personal situation is advised to seek out a qualified advisor or advisors and provide as much information as possible to the advisor in order that such advisor can take into account all relevant circumstances, objectives, and risks before rendering an opinion as to the appropriate strategy.

Be the first to know about new articles, series and events.

Your cart is currently empty!

Notifications