Are Taxpayers Helping to Finance America’s Data Center Boom?

A Quest for Clarity

June 22, 2026

No posts

“Government is the great fiction through which everybody endeavors to live at the expense of everybody else.”

~ Frédéric Bastiat

By Taylor Hudak

A strikingly large number of massive data centers are being built across the United States. It is currently estimated that there are more than 4,000 data centers in the U.S., and more are on the way.

The federal government as well as local and state governments are providing financial incentives for these investments. Such incentives occur in an environment that lacks transparency and proper disclosure. As an extension of this opaqueness, the benefits to justify these subsidies also remain unclear. Many would argue that promises of job creation have been grossly overstated (and the data centers’ potential role in creating a digital control grid kept secret), while energy and resource concerns—as well as the potential costs of site cleanup if and when the facilities close down or fail—have been minimized. This, in addition to the secrecy surrounding the planning and financing of the data center industry, indicates that the negative impact to local residents and the American taxpayers may be substantial.

The following report examines this matter and is organized into two main sections. The first covers the federal layer of financial influence helping to advance the data center boom—the One Big Beautiful Bill. The second section focuses on the generous state and local government tax incentives, which are costing state governments billions in revenue losses. The conclusion elaborates on an opportunity to join the effort in seeking clarity on America’s data center industry, with additional resources provided in the links below.

The One Big Beautiful Bill (OBBB), signed into law on July 4, 2025, impacts the Internal Revenue Code (IRC) and includes significant changes to business tax incentives, among other things.

It is important to make clear that the OBBB does not specifically mention data centers, nor does the legislation appropriate a single dollar for them. There is no vote to fund the industry, no line item, and thus, there is nothing to oppose. Yet, the OBBB is one of the most significant data center policies enacted in the United States. “The government isn’t funding data centers,” says Attorney Anthony Parent, an American tax lawyer who advises on business tax planning and Internal Revenue Service (IRS) controversy. “It’s declining to tax the people who build them—which feels identical to everyone except the lawyers.”

This is the mechanism of the tax expenditure—it is money the government declines to collect rather than money it chooses to spend. It never appears as a budget line, and it requires no appropriation. In Atty. Parent’s assessment, it is a subsidy that the public rarely sees because it does not look like spending.

There are three ways in which this tax expenditure works as permitted by the OBBB in relation to the data centers:

The most consequential provision applied to the data centers is the amendment to Section 168(k) of the IRC found in OBBB Section 70301. The new rule restores 100% bonus depreciation for equipment purchased after January 19, 2025.

Typically, when a business purchases expensive equipment, it cannot deduct the entire cost immediately. It spreads the deduction across several years—a process called depreciation. The amended Section 168(k) allows businesses to deduct the full cost in Year One. The advantage for firms is that they are reducing their profits by the amount of depreciation and hence they are also reducing their tax bill.

For data centers, this is very beneficial because it applies to the most expensive part of the data center—the chips.

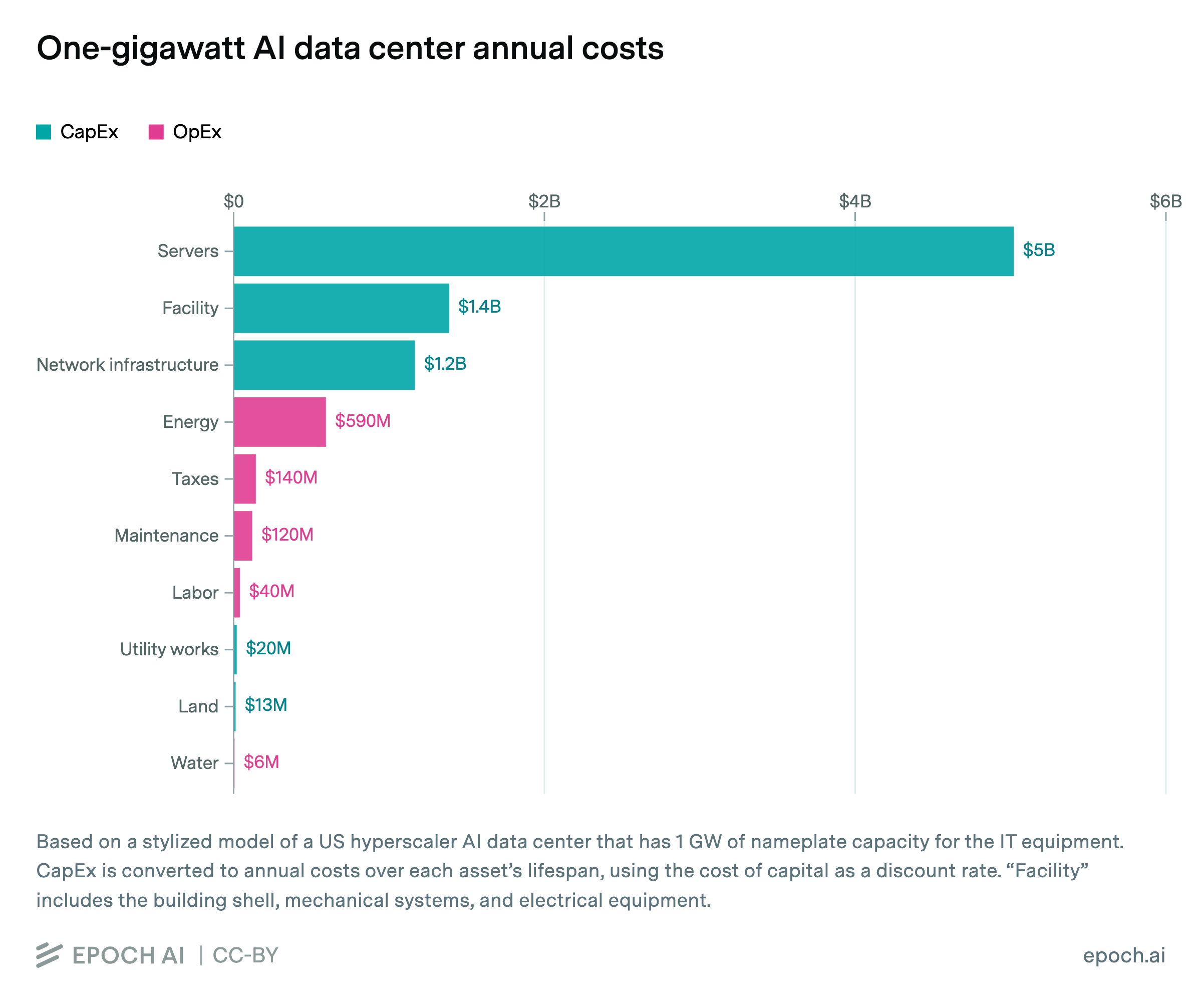

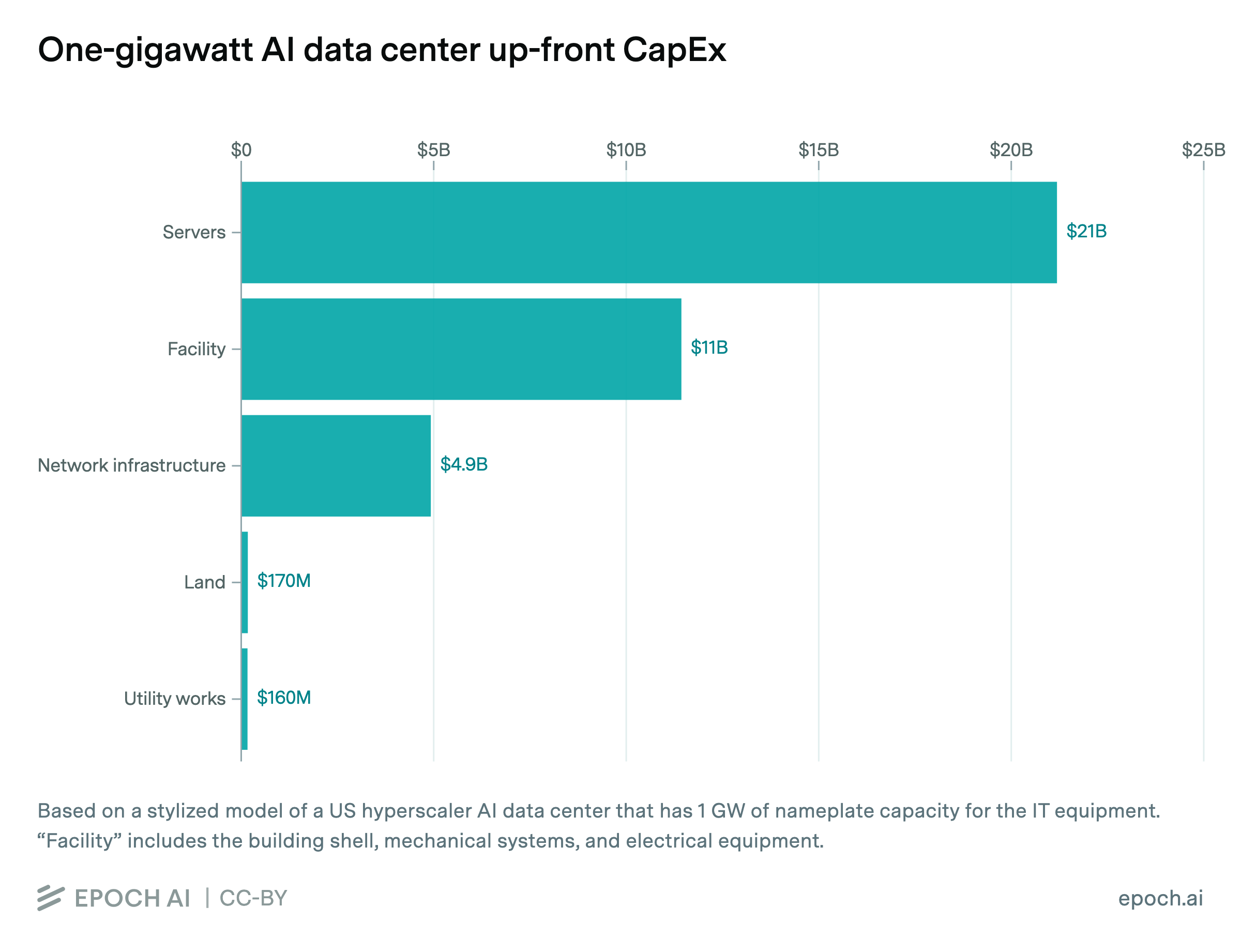

According to a cost breakdown published by Epoch AI, servers account for 60% of the total cost of ownership (TCO) of a typical one-gigawatt data center. The report estimates that an average data center requires $38 billion in up-front capital expenditure (CapEx) and $8.5 billion per year in total annualized cost—of which servers alone account for $5 billion annually.

Meanwhile, operating costs, including energy, are much smaller in comparison. Utility works, land, and water combined make up only $39 million of the total annual CapEx and Operating Expenditure (OpEx).

The building itself, by comparison, is relatively inexpensive and does not qualify for bonus depreciation under amended Section 168(k). However, the chips and server hardware do qualify.

Atty. Parent says, “Sixty cents of every dollar spent goes toward the chips—which are also given the biggest tax break. That’s the cleanest version of the giveaway: the tax break is biggest on the most expensive, fastest-obsolete part of the project.”

The most expensive components, the hardware and IT equipment, must also be replaced and repurchased every three to five years, on average. Under amended Section 168(k), a new full deduction applies each replacement cycle. The building requires renovation approximately every 14 years and, as mentioned, does not qualify for bonus depreciation under amended Section 168(k).

Thus, in summary, the tax code has effectively structured the incentives to sit precisely on the components that cost the most, depreciate the fastest, and must be repurchased most frequently.

The second provision that impacts the data centers is the new Section 168(n) established in OBBB Section 70307. This subsection allows a business to deduct the entire cost of a qualified production property (often referred to as QPP)—a factory or manufacturing facility—in Year One rather than throughout a 39-year depreciation schedule.

Initially, this provision appears to be a direct data center break, given that it covers large facilities, offers immediate deductions, and thus, at first, seems to be an obvious fit. However, it is not that simple.

To meet the criteria as a qualified production property under Section 168(n), the facility must be used to manufacture, produce, or refine a tangible product. Data centers process data, which is intangible. IRS Notice 2026-16, issued in February 2026, ties eligibility to manufacturing industry codes that data centers do not fall under.

Atty. Parent explains, “Congress wrote a special break for factories that physically make things. A data center makes data. It probably doesn’t qualify—but it didn’t need to, because the equipment break already did the work.”

Where Section 168(n) does benefit the data center build-out is one step back in the supply chain. Semiconductor fabrication plants, or chip fabs, manufacture the physical chips that data centers rely on. Therefore, these chip fabs produce tangible property and almost certainly meet the criteria as qualified production property under Section 168(n).

Put simply, as prescribed in the OBBB, amended Section 168(k) subsidizes the purchase of chips for the data center. The new Section 168(n) subsidizes the factories that manufacture those chips. The incentives run through the entire supply chain without ever naming the industry they benefit.

A data center is not just one investment. “A data center is really two assets with two completely different tax treatments—and that quietly decides who invests in each half,” says Atty. Parent.

The first half is the expensive, fast-depreciating half, which includes the chips, the servers, and the cooling equipment. This is an income-tax play. The bonus depreciation under amended Section 168(k) creates immediate deductions that attract operators and high-income investors who need losses to offset current income.

The second half is the appreciating half, which includes the land, the building, the power access, and the grid connections. These assets are relatively inexpensive to acquire and have long-term durability. They cannot be written off quickly and do not benefit from Section 168(k) bonus depreciation. However, these assets do qualify for a different set of tax advantages such as capital gains treatment, like-kind exchanges under Section 1031, and Opportunity Zone investments.

Furthermore, the OBBB permanently renews and expands the Opportunity Zone Program, which was first enacted under the Tax Cuts and Jobs Act (TCJA) of 2017. Opportunity Zones provide capital gains tax exemptions for investments in designated lower-income areas. The OBBB extends the program indefinitely and introduces a new category, the Qualified Rural Opportunity Funds (QROF) that offer even greater tax benefits for investments in rural areas, which is defined as any area outside a city or town with a population greater than 50,000.

Data centers are land-intensive and power-intensive. They are being built in rural areas and in smaller markets precisely because the land is cheap and the power infrastructure is available. Many of those locations will qualify as Opportunity Zones or rural opportunity areas under the OBBB’s expanded program.

The tax code has effectively divided the investment in a data center into two streams—a depreciation stream for the hardware-focused investor and a capital gains stream for the real estate-focused investor—and provided a different incentive for each.

The picture is not entirely favorable for data centers. The OBBB also accelerated the wind-down of solar tax credits and ended an energy-efficiency deduction that data centers had been using.

“Claiming the OBBB is a data center giveaway is too simple,” says Atty. Parent. “It is a giveaway on the equipment side and a clawback on the energy side.”

Data centers consume significant amounts of power. Atty. Parent explains that the clean energy credits that were helping operators offset energy costs have been reduced or eliminated. The industry that benefits most from the equipment provisions is simultaneously losing the incentives that were making its power consumption more financially manageable.

The OBBB is arguably the most complex piece of tax legislation in recent history. It was enacted at a time in which the IRS is facing significant institutional instability. The IRS has no confirmed Commissioner, its workforce is down 25% from cuts, and a Supreme Court decision in Loper Bright Enterprises v. Raimondo narrowed the IRS’s authority to interpret the very tax provisions that are now expanding.

“More tax complexity being built with one hand, while the agency that enforces it cracks in the other,” says Atty. Parent. “Nobody is putting those two facts on the same page.”

He suggests that the simultaneity is the story. A law that creates new categories of deductions, new opportunity fund structures, and new manufacturing incentives—all requiring interpretation, guidance, and enforcement—landed in the hands of an agency that is simultaneously losing the legal authority to interpret it and the personnel to enforce it.

State tax abatements add another layer. Data center investments receive substantial additional subsidies at the state level through sales-tax exemptions and property-tax abatements. According to a June 2026 report in Good Jobs First, several states are already losing more than $1 billion per year in revenue from data center tax breaks. Meanwhile, comprehensive data remain difficult to obtain because 14 of the 37 states with relevant exemptions do not properly disclose their revenue losses.

“This is central planning,” says Atty. Parent. “It only gets called patriotism because it runs through the tax code instead of a communist chairman’s five-year plan.”

The specifics of the state and local-level policy implementation and reporting and compliance guidelines do slightly vary state to state. Yet, the data indicate there are very clear themes observed across all the states. Recent developments in Ohio serve as a helpful example to understand what is occurring more broadly in other regions across the country.

The state of Ohio has considered a bill aimed at reducing massive sales-tax exemptions for companies involved in the data center industry. Ohio House Bill (H.B.) 646 received bipartisan support and eventually passed the Ohio House in March 2026. The legislation would have reduced sales-tax exemptions on the purchase of materials and equipment by large companies for data centers from 100% to 50%. However, after H.B. 646 reached the Ohio Senate and underwent significant revisions, some Democratic and Republican lawmakers opposed the final, revised version of the proposed legislation, which included revisions adjusting the tax exemption rate from 50% to between 50% and 75%.

There was also mention of non-disclosure agreements (NDAs) in the substitute bill, but it did not include a constructive ban on such agreements. NDAs and other confidentiality clauses have been used in other state and local government data center proposals and planning initiatives. Eventually, in June 2026, substitute H.B. 646 did not pass the Ohio House. The Ohio House intends to reconvene again at the end of June to attempt to reach a compromise.

Specifically, H.B. 646 aimed at reducing a lesser-known, and now rather controversial, tax exemption which was introduced in the mid-2010s under then-Governor John Kasich. The tax benefit allowed a 100% sales-tax exemption for companies purchasing equipment for data centers.

However, H.B. 646 would not apply to companies with existing contracts like Meta, Google, and Amazon—whose contacts, which include the tax exemptions, are in effect for 40 years. The bill would only apply to new companies seeking a contract in Ohio, and even then, the sales-tax exemption would not be eliminated but rather reduced by 50%. What’s more, the costs to the state due to these tax exemptions are already extremely high and are very hard to predict. And this does not apply to just the state of Ohio.

According to a news report, Ohio state officials’ estimates for sales-tax exemption costs for the year 2025 were wildly off. Instead, the actual costs were more than 10 times greater than predicted, reaching almost $1.6 billion in sales-tax exemptions for the purchase of data center equipment and materials. Another news report published in May 2026 cites Ohio Department of Taxation data (presumably the same data examined in the previously mentioned report). According to the article, the revenue losses increased dramatically in just one year. A year prior, in 2024, the state lost $555 million and localities lost $166.8 million in revenue. Good Jobs First claims these figures indicate that Ohio has one of the most expensive subsidy programs in the nation.

After it became public that Ohio’s Department of Taxation underestimated the costs of the data center tax exemptions by more than $1 billion, Ohio Governor Mike DeWine paused the sales tax break for data center companies at the end of May 2026. Yet, given that the proposal, H.B. 646 failed, Ohio’s 100% sales-tax exemption will still apply to new companies seeking a data center-related contract in the state. Despite the U.S. Congress adjourning for summer recess, the Ohio House expects to meet at the end of June to reach a compromise.

While seemingly specific, predicaments like the one described for Ohio are experienced all across the country. For many states, like Ohio, the common trend is generous tax exemptions for mega corporations, followed by billions in lost tax revenues by state governments, and the inability to accurately predict projected costs due to a lack of transparency and compliance in the reporting.

These points, and others related to the impact of the data center rush, are presented in a series of financial analyses published in Good Jobs First, an American policy research center that promotes government and corporate accountability in the area of economic development. Founded in 1998, Good Jobs First, a non-profit entity, advocates for transparency in the use of public money. The organization has closely tracked various aspects of the data center industry as it pertains to local and state governments.

The following section references three in-depth financial research reports published by Good Jobs First—one released in April 2025, a second in April 2026, and a third in June 2026. All three reports examine common issues surrounding the data center industry observed at the state and local levels. This includes, but is not limited to, tax abatements (including property tax abatement), non-compliance, and lack of transparency, as well as state tax revenue losses and future trends.

First, it is important to understand that there are varying degrees of disclosure regarding tax abatement-related revenue losses:

Some states do not disclose at all, including Alabama, Arkansas, Idaho, Indiana, Iowa, Louisiana, Maryland, Mississippi, Missouri, North Carolina, North Dakota, Oklahoma, South Carolina, and Utah.

A few states disclose in their Annual Comprehensive Financial Reports (ACFRs), including Texas, Virginia, and Washington.

Some states also or only disclose in their Tax Expenditure Reports (TERs), including Arizona, Connecticut, Florida, Georgia, Kentucky, Michigan, Minnesota, Nebraska, New York, Ohio, Pennsylvania, Tennessee, Texas, Washington, West Virginia, and Wisconsin.

The information about tax abatement disclosure is from a chart published in April 2026 by Good Jobs First. In the same April 2026 report, which is focused primarily on the “too-often undisclosed ways [the data centers] take taxpayer funds in the form of tax abatements,” it is important to note that the tax-abatement laws applying to the data centers predate the existence of the large Artificial Intelligence-driven data centers being built today. Thus, these tax-abatement laws were written for much smaller facilities and at a time when cloud-computing server farms were much smaller.

In its April 2025 report, Good Jobs First examines the data centers’ impact on state budgets. According to the report, the figures at the time indicated that “at least 10 states lose more than $100 million per year in tax revenue to data centers.” The report also notes that accurate cost projections are difficult given the data center industry’s high-velocity growth combined with the state tax exemptions.

At the time the report was published, Good Jobs First estimated that the actual losses are likely far worse than they are able to document, given that 12 of the 32 states (with tax incentives for data center business infrastructure) fail to disclose aggregate revenue losses. Three of those 12 states are Indiana, North Carolina, and Utah, each of which has significant data center investments. Today, most Americans are familiar with the Box Elder County, Utah, data center, which has been the subject of much controversy and is expected to be the largest data center (aspiring to cover 40,000 acres) in the country.

In its report, Good Jobs First then outlines what they argue is a disclosure compliance issue regarding tax exemptions for companies facilitating the development of data centers. They consider the data center tax exemption/s to meet the definition of “tax abatement” as it is outlined in Statement No. 77 on Tax Abatement Disclosures of the Governmental Accounting Standards Board (GASB) of the Generally Accepted Accounting Principles (GAAP).

GASB Statement 77 requires the existence of an agreement between a government and an entity or an individual, in which the government agrees to receive less tax revenue in exchange for that individual or entity providing a positive economic impact on the state such as job creation. If such an agreement is made, then the resulting tax revenue losses meet the GASB definition of a tax abatement, and thus it is required to disclose the loss in GAAP-compliant jurisdictions. The 2025 Good Jobs First report explains that the tax exemptions meet the tax abatements definition because “they involve an agreement between a state and a data center company in which the state agrees to forego income in exchange for the company doing something (such as investing and/or hiring) that the state deems beneficial.”

One year later, Good Jobs First shared the application forms in a report proving that states are, in fact, seeking eligibility for “sales and use tax exemptions on building materials and/or equipment and/or utility charges.” They argue that this makes it clear that state governments and companies are making agreements, which then qualifies the tax exemptions as “tax abatements,” and, therefore, there is an obligation to disclose revenue losses.

Based on this, the Good Jobs First suggests that each state and each local government that uses GAAP and also experiences revenue losses due to data center tax abatements should disclose those revenue losses in their Annual Comprehensive Financial Report.

Additionally, as Good Jobs First reported in April 2026, 14 states and several local municipalities still fail to disclose revenue losses. Based on the information provided from the states that do the proper reporting, losses are rapidly increasing. In some instances, revenue losses have reached beyond $1 billion per year. Whether there are even higher losses and worse estimates in some non-reporting states is a reasonable question. According to the report, these states “are almost certainly hiding massive and sharply escalating budget-busters.” In the case of Indiana, the Indiana Economic Development Corporation (IEDC) and state Comptroller’s office have since revealed additional data, which show significant losses of nearly $700 million to data center tax exemptions in 2025.

As previously mentioned, in the states that do disclose, the trend shows that losses are continuing to increase. Despite this, according to the organization’s June 2026 report, “comprehensive and up-to-date data on subsidy costs remain limited…. [S]ome states do not publish costs annually, and 14 of the 37 states with sales and use tax exemptions for data centers do not publish their official revenue losses at all in a timely matter.” Therefore, this presents larger issues. The lack of disclosure combined with rapid industry growth makes it difficult to accurately determine the costs of data center subsidies or produce a complete cost-benefit analysis.

Furthermore, the companies running the data centers routinely stack subsidies that often do not have caps on the total tax-break benefit for any given data center. Thus, these companies simultaneously collect sales tax exemptions, property tax abatements, and income tax credits that do not favor job creation but rather capital investment, according to the findings.

Property tax abatements are also often applied to data center companies at the local level. According to the Good Jobs First June 2026 report, property tax abatements are typically very costly, given that property taxes are the largest form of state or local tax a corporation owes. However, it is often difficult to track property tax abatements as they are typically negotiated on a case-by-case basis and only a few states maintain centralized databases that include local property tax abatements. With more data centers, the cost of property tax subsidies increases.

The report cites two examples in which property tax abatement information is disclosed and easy to access—in Oklahoma and Oregon. In both states, the findings demonstrate that the major tech companies are receiving millions in property tax abatements. For example, and to put this into perspective, in Oregon between 2016 and 2023, four tech giants (Amazon, Meta, Apple, and Alphabet) received approximately $615.8 million in property tax abatements.

Although information on property tax abatements is generally difficult to find and access, these data were obtained either through elected officials’ public statements or through individual lawmakers, journalists, and civil society members submitting public records requests. Put simply, when members of the community become engaged with the issue, they can get the results that they want—the answers and more information.

Given that the cost of tax subsidies for data centers is not fully disclosed in many states, it is often impossible to ascertain the benefits against the costs to the average taxpayer. Furthermore, one must ask, what are the perceived benefits?

Some states have explained their tax abatement policy by referring to benefits in terms of job creation. However, in comparison to the telephone call center boom in the 1980s and ‘90s, data centers are not even creating low-level jobs. With staffing at data centers expected to be minimal, the benefit of job creation to justify massive tax exemptions for corporations is questionable. To further complicate the matter, many states have not presented a transparent case for their cost-benefit assessment that could be used to check if the subsidies actually benefit the public.

In addition to costs in the form of lost tax revenues, there are many other potential costs to society with the establishment of many large-scale data centers, including the possibility of reduced local access to electricity and the water supply, especially if data centers are prioritized. This means that locals either lose access to such resources, or alternatively, access is much more expensive. These increased costs would also have to be held against any perceived benefits.

Thus, if the benefits do not exceed total aggregate costs, including tax and societal costs, then states are not justified in granting tax rebates and subsidies to companies involved in the data center industry. This could explain states’ failure to disclose certain data and their lack of transparency on such issues.

While the data center boom in America has generated significant public interest and concern, we have yet to reach a full understanding of how the costs, the use of resources, and the tax incentives will impact our daily lives and the functioning of our local communities and state and national governments. Even in an environment that lacks transparency, the data that are accessible indicate that the tax incentives for companies engaged in the data center industry are costing states millions and billions of dollars.

These facts leave no question about the potential impact this industry may have. However, in several local communities throughout the U.S., there have been cases in which citizens successfully have pushed back against the data center build-out. Take, for example, the state of Florida, where in May 2026 Governor Ron DeSantis passed an AI data center law. Many would argue against this new law, yet it does include a provision which preserves the local governments’ authority over planning and land development regulations. As a result, several counties have already implemented permanent bans on AI data centers or are seeking to restrict or delay building and planning, reflecting the sentiment and attitudes of many Floridians.

This is why it is essential to push back against the local governments signing NDAs that keep data center plans and negotiations secret from local citizens until it is too late for them to stop a deal that is bad for the local community. In her report for Solari titled Mr. Global in Your Street, Elze van Hamelen suggests the time has come for citizens to crowdfund a local reporter or other local resident to carefully track local municipal budgets, contracts, and negotiations. This can provide an early warning system to busy local business leaders and farmers, ensuring that they learn about instances where their tax dollars are being invested in a way that will harm their business or their personal finances and health.

The massive Box Elder County data center facility in Utah, expected to cover 40,000 acres, has received strong and vocal opposition from members of the community through attendance at city council meetings and protests. Likely as a result, the Box Elder County commissioners approved a broader effort to limit the data center industry in Utah in the form of a 180-day moratorium on new data centers and data center power plants in the county. With regard to the specific Box Elder County data center, it has been reported that Kevin O’Leary, the main investor, must significantly reduce the size and scale of the project.

Both the Florida and Utah examples demonstrate that the opportunity to initiate positive change and redirect the course of events is upon us now. Developing a clear financial map and outlining the major sources and types of funding driving this data center boom are of great importance. Given that the industry is vast, multifaceted, and rapidly developing, we welcome your assistance in our efforts to seek clarity. If you have any relevant insights, personal experience, or expertise that may assist in determining who and what is funding and advancing the data center boom in America, we kindly encourage you to email more information at intel@solari.com. Solari hopes to continue this series by next taking a look at how our private savings and pension funds are being used to finance data centers.

The links below include selected reports, including articles and videos, that provide further information and analysis pertaining to the data center industry not otherwise covered in this report. (Disclaimer: The views expressed do not necessarily represent the views of Solari.)

Tucker Debates Kevin O’Leary on AI, American Jobs and the Fall of the American Empire (The Tucker Carlson Show, May 13, 2026)

The Data Center & Smart City Connection | Daily Pulse Ep 271 (Maria Zeee at Zeee Media, June 12, 2026)

Virginia Neighbors Fed Up with Constant Hum (Brian Entin’s News Nation, June 19, 2026)

Timeline: How the Kevin O’Leary Data Center Plan Came to Be, and What’s Happened Since (The Salt Lake Tribune, May 19, 2026)

Private Equity: See the Game, Change the Game with Tiffani Cianci (January 6, 2026)

Update on the Trouble in Private Credit with Tiffany Cianci (March 24, 2026)

Lunacy Threatens 401(k) and Index Fund Regulation with Tiffany Cianci (June 23, 2026)

Pushback of the Week: May 31, 2026: Data Center Opponents Exploit a Loophole

Already a subscriber?

Our mission is to help you live a free and inspired life. This includes building wealth in ways that build real wealth in the wider economy. We believe that personal and family wealth is a critical ingredient of both individual freedom and community, health and well-being.

Nothing on The Solari Report should be taken as individual investment, legal, or medical advice. Anyone seeking investment, legal, medical, or other professional advice for his or her personal situation is advised to seek out a qualified advisor or advisors and provide as much information as possible to the advisor in order that such advisor can take into account all relevant circumstances, objectives, and risks before rendering an opinion as to the appropriate strategy.

Be the first to know about new articles, series and events.

Your cart is currently empty!

Notifications